Ghana has built a fintech ecosystem of genuine distinction within the sub-region. Digital payments have expanded more than 11,000 times over the past decade. The country ranks first globally on the GSMA Mobile Money Regulatory Index and has surpassed its own financial inclusion targets. These outcomes reflect deliberate policy, sustained institutional investment, and a regulatory posture that has been both progressive and enforceable.

Yet the evidence demands a more considered assessment. Access to financial services is not equivalent to financial depth. Ghana has largely resolved the access problem. It has not resolved the depth problem, and that distinction carries substantial economic consequence.

Inclusion Has Expanded. Depth Has Not.

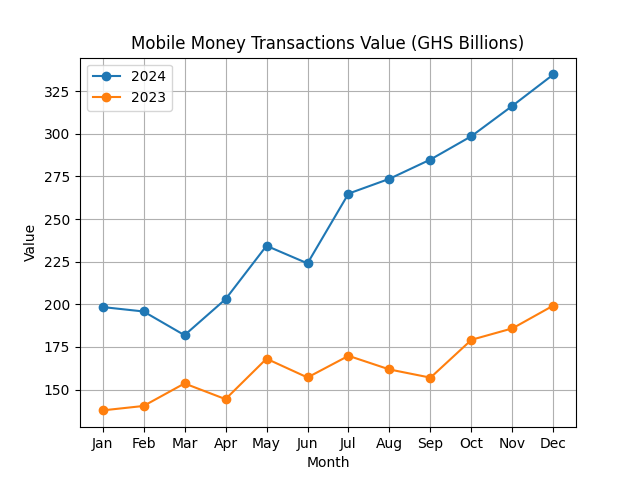

Ghana’s informal economy generates the majority of daily economic activity yet remains largely invisible to the formal credit system. Only 16 percent of adults are covered by credit bureaus. Digital financial services contributed an estimated 4.5 percent to GDP in 2024, modest despite extraordinary transaction volumes.

Transaction throughput is not economic transformation. Credit, savings mobilisation, insurance, and investment are the mechanisms through which financial systems generate sustained economic value. Ghana’s fintech ecosystem remains significantly underdeveloped across each of these dimensions beyond payments.

Mobile credit has expanded the boundaries of formal borrowing, but primarily through short-tenor, high-cost, unsecured instruments. These are not structurally equivalent to the patient capital required to finance enterprise growth or long-term household development. A financial system where the majority of formal borrowers rely exclusively on mobile nano-credit has not achieved credit market development. It has digitised credit exclusion.

The Payment Infrastructure Is Coherent. The Ecosystem Is Not Balanced.

Ghana’s interoperable payment infrastructure is among the sub-region’s more coherent institutional achievements. GhIPSS provides the foundational settlement infrastructure that makes cross-provider interoperability viable. GhanaPay and a standardised national QR framework have reduced fragmentation across the ecosystem.

A candid evaluation, however, reveals a concentration of activity that demands strategic attention. Payment services dominate to the relative exclusion of other verticals. Digital lending, insurtech, wealth management, and B2B financial infrastructure remain underdeveloped relative to the transaction volumes the payment layer now generates. The next phase depends on directing capital toward these verticals, not sustaining the momentum of what has already been achieved.

The Second Wave Requires Building Above the Rails

The maturation of Ghana’s payment infrastructure creates both the opportunity and the imperative to build the financial services layer above it. Digital wallets are transitioning from payment instruments toward financial hubs incorporating credit, savings, insurance, and investment services. The technical conditions for this transition are being established.

GhIPSS is developing an API for real-time Ghana Card verification in lending decisions. When a market trader with years of consistent mobile money history can present a verifiable national identity to a licensed lender, the economics of extending credit to previously unscored populations change fundamentally. The barrier is not risk. It is information asymmetry, and that asymmetry is addressable.

The Bank of Ghana’s Open Banking Framework, currently in proof-of-concept, will enable consent-based data sharing between banks, fintechs, and regulated third parties. Open banking is not primarily a technological initiative. It is an institutional one. It is the mechanism through which Ghana’s payments data becomes the foundation for a scalable credit infrastructure. The policy will is present. What is now required is the implementation discipline to deliver a framework institutions can build upon with confidence.

Five Priorities to Convert Payment Scale into Financial Depth

Accelerate Ghana Card integration into financial infrastructure. The technical specifications are established. Every period of delay perpetuates the information asymmetry that prevents creditworthy Ghanaians from accessing affordable capital.

Publish a binding open banking framework. Strategic commitment must translate into published API standards, accreditation criteria, and an implementation schedule against which regulated institutions can plan and invest.

Direct public capital toward infrastructure rather than products. The most durable returns will derive from investment in shared credit infrastructure, interoperable identity systems, and open data utilities, not direct support for consumer-facing lending products.

Build a regulatory framework designed for B2B fintech. Embedded payments and working capital facilities serve a different risk profile and commercial logic than consumer lending. Applying consumer regulation to B2B fintech without adaptation creates compliance friction and may constrain a segment with significant productive potential.Sustain momentum on virtual assets regulation. Following the Virtual Asset Service Providers Act enacted in December 2025, Ghana established a regulatory first-mover position in West Africa. That advantage depreciates if implementation does not match legislative ambition.

Regulatory Design Shapes Market Outcomes

Global benchmarks make this clear. Brazil’s PIX, built and operated by the central bank with mandated interoperability, surpassed 140 million users within three years. India’s UPI combined public rails with open API access to enable ecosystem-wide competition. Scale follows regulatory design, not market momentum alone.

Ghana’s legislative record is substantive. The Payment Systems and Services Act, the Digital Credit Services Directive, and the Virtual Asset Service Providers Act collectively constitute a regulatory architecture few West African jurisdictions can match. From November 2025, digital credit providers must obtain licences, maintain minimum capital thresholds, submit credit data to bureaus daily, and comply with consumer protection standards.

The determinative question is no longer whether Ghana has appropriate regulation. It is whether regulation is being implemented at the pace the market demands. The Ghana-Rwanda fintech passporting agreement, Africa’s first such bilateral arrangement, provides a model for what regulatory cooperation can produce. If it demonstrates operational viability, Ghana will have authored the template other markets seek to replicate.

Three Questions That Will Define the Decade

Will Ghana build the credit infrastructure commensurate with its payments achievement? The foundations exist. What is required is the institutional urgency to complete them.

Will Ghana’s first-mover regulatory advantage in digital assets and open banking convert into durable market leadership? Nigeria commands a larger market. Kenya has a more mature venture ecosystem. Rwanda is advancing open banking with notable commitment. Ghana’s advantage resides in the quality of its regulatory environment, and that advantage is not self-sustaining.

Will Ghanaian fintech enterprises build for the West African region or only for the domestic market? The Ghana-Rwanda passporting agreement and the virtual assets sandbox position Accra as a potential regional hub. Realising that opportunity requires founders, investors, and regulators to orient toward the 400 million people of ECOWAS, not merely the domestic consumer base.

Ghana has built the rails. The strategic task now is to ensure those rails lead to depth. The institutions that execute this transition with the necessary urgency and coherence will not merely improve Ghana’s financial sector performance. They will establish the model that defines West African fintech development for the decade ahead.